1.Introduction

Since the 19th century, Argentina has experienced multiple external debt crises. Considering the scale and impact of certain external debt crises, attributing Argentina’s external debt problem solely to economic fluctuations is not enough to explain this recurrent and complex structural problem. Therefore, it is necessary to further analyze Argentina's external debt crisis. Since the economic, historical, and political factors vary in different debt cycles, the author chooses to use the representative 2001 external debt crisis as a case for analysis.

In 2001, the Argentine president announced a moratorium on repayment of US$132 billion in external debt, marking the outbreak of this external debt crisis [1]. During this crisis, the total external debt reached US$152.6 billion and the proportion of external debt to Gross National Income (GNI) reached 159.9% [2]. The 2001 external debt crisis profoundly impacted Argentina's economic development, financial markets, economic policies, and even economic development patterns. After the external debt crisis outbreak, Argentina's Gross Domestic Product (GDP) index fell sharply. In 2002, Argentina's GDP growth rate was -9.32% [3]. The hyperinflation and surge in unemployment rates led to further poverty and a decline in the national living standards. At the same time, the government's fiscal deficit expanded, leading to the government's reduction in welfare spending, which led to a further decline in the national living standards.

The foreign debt crisis directly triggered panic in the capital market, with substantial amounts of capital fleeing and even bank runs. The Argentine government finally had to implement financial controls to restrict capital flows. To obtain aid loans from the International Monetary Fund (IMF) to solve its debt problem, the Argentine government needs to accept the IMF's supervision and restrictions on its economic policies and give up some of its economic sovereignty. Finally, the external debt crisis directly affected Argentina's economic development patterns. After the new government came to power in 2002, it announced the abolition of the currency board system, and at the same time strengthened financial controls and restricted capital flows, marking the bankruptcy of the neoliberalism that had been implemented since the 1990s. Since then, Argentina has begun a difficult transformation.

External debt itself is neutral, but when a country has a serious external debt crisis, it means that there are unreasonable economic and financial structures and unsustainable development patterns behind the external debt problem. Therefore, proposing a reasonable response strategy can not only solve the negative impact of the external debt crisis on the economy but also help to build a sound financial system and a healthy development pattern. The historical roots of Argentina's external debt crisis are mainly the following four aspects: unreasonable economic structure, fixed exchange rate lacking flexibility under the currency board system, extensive privatization reform, and long-run fiscal deficit. Based on this, this paper aims to take the 2001 external debt crisis as a case to explore the causes and historical roots of Argentina's external debt crisis and analyze what measures the government can take to deal with the external debt crisis.

2.Historical Background of Argentina's External Debt Crisis

The historical background of Argentina's external debt crisis can be divided into two parts: domestic and international. The domestic perspective can be interpreted from three aspects: economic background, political background, and debt accumulation. In terms of economic background, Argentina began to implement neoliberal reforms in the 1990s. The core content was the currency board system and market liberalization. The new government further opened up the capital market, abolished foreign exchange controls, and implemented a fixed exchange rate of 1:1 between the new currency peso and the US dollar. Besides, the issuance of the peso was based on the US dollar foreign exchange reserves [4]. These measures reduced the inflation level but also made the Argentine government lose the independence and flexibility of monetary policy. When the foreign trade and international financial environment changed, Argentina could only passively bear the impact. In addition, Argentina has a huge fiscal deficit. Due to its unreasonable fiscal structure, there is too much welfare expenditure and not enough production expenditure in fiscal expenditure. During the reform process, the excessive and extensive promotion of nationalization to privatization caused the government to lose its long-term source of tax revenue.

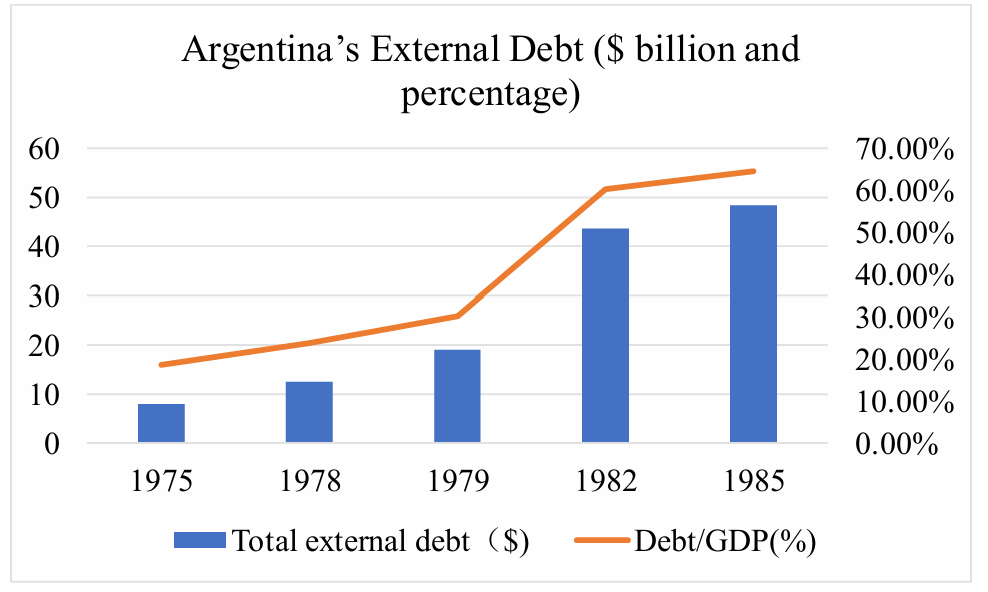

In terms of political background, Argentina was ruled by a military dictatorship from 1976 to 1983. During this period, the military government cracked down on Peronists and relaxed control over the economy, which also generated a large amount of external debt. In 1983, the new government came to power. Although it actively negotiated with the IMF and other organizations for certain international aid, the domestic debt problem was still not resolved. In 1989, the Peronist Party, with national rejuvenation, national liberation, and centralization as its platform, returned to power and promoted a series of free market reforms. In terms of debt accumulation, after 1978, due to the expansion of the fiscal deficit, the growth rate of external debt increased significantly. According to data provided by scholars such as Rudiger Dornbusch, Argentina's external debt crisis gradually became more serious, as shown in Figure 1 [5].

Figure 1: Argentina’s External Debt ($ billion and percentage)

From the perspective of the international environment, the performance of the US dollar in the currency market has a direct impact on the Argentine economy. Since the peso is pegged to the US dollar, the fluctuations of the US dollar in the currency market are directly transmitted to the Argentine economy, causing the peso to remain overvalued for a long time. At the same time, although the overvalued peso has attracted a large amount of international capital, the capital flowing into the country through arbitrage behavior has also increased Argentina's financial risks. Once the market situation of the US dollar changes dramatically or the serious overvaluation of the peso causes market panic, a large amount of foreign capital will flee and trigger a financial crisis. In addition, Brazil is Argentina's main trading partner. When the financial crisis broke out in Brazil in 1999, the authorities implemented a strategy of drastically devaluing the currency which had a huge impact on Argentina's economy and finances and worsened Argentina's external environment [6].

3.The Details of the 2001 Argentina External Debt Crisis

The following will combine data to analyze Argentina's 2001 external debt crisis from the aspects of external debt scale, external debt structure, and debt restructuring. According to the data of the World Bank, Table 1 can be obtained [2].

Table 1: Argentina's total external debt and its ratio to GNI

|

Years |

Total external debt(billion/current$) |

Total external debt (Percent of GNI) |

|

1995 |

98.77 |

39% |

|

1996 |

111.15 |

41.7% |

|

1997 |

128.25 |

44.7% |

|

1998 |

141.5 |

48.5% |

|

1999 |

151.91 |

55% |

|

2000 |

150.06 |

54.2% |

|

2001 |

152.65 |

58.5% |

|

2002 |

148.32 |

159.9% |

|

2003 |

163.44 |

133.5% |

|

2004 |

168 |

114.8% |

|

2005 |

130.79 |

74.2% |

The scale of debt can directly reflect the degree of debt repayment pressure. As can be seen from Table 1, Argentina's external debt increased from US$98.7 billion in 1995 to US$152.6 billion in 2001, and its proportion in GDP soared from 39% to 159.9%. It is worth noting that, the ratio of debt to GDP/GNI can intuitively reflect the country's debt repayment pressure and debt risk. However, as for Argentina's external debt, although the scale of external debt fell in current US dollars from 2001 to 2002, its proportion in GNI increased significantly. This ratio does not mean that Argentina's debt level reached 150% of GNI. Considering that most of Argentina’s debts in this external debt crisis are denominated in US dollars. When anti-inflation debt is denominated in foreign currencies, it will be adjusted through the price index of foreign currencies and the nominal exchange rate between domestic and foreign currencies. The conclusion drawn from this is that changes in the ratio of external debt to GNI are not only related to the size of the deficit but also to changes in relative prices.

From the perspective of external debt structure, in terms of currency structure, Argentina’s external debt is mainly dominated by the US dollar. The excessive proportion of U.S. dollars reduces Argentina's ability to resist risks in its external debt. When the U.S. dollar appreciates in currency markets, it will significantly increase Argentina's debt repayment risk. In terms of debt repayment period, most of them are concentrated in the period 2001-2004 [1]. Leading to excessive debt repayment pressure in a specific period and increased risk coefficients

In terms of debt restructuring, after the outbreak of Argentina's external debt crisis in 2001, the most direct impact was that the Argentine government was not allowed to borrow in the international market due to debt default. Afterward, the Argentine government launched two rounds of debt negotiations in 2005 and 2010. The two rounds of negotiations completed the restructuring of 75% and 18% of the debt respectively [7]. The remaining creditors were mainly composed of "vulture funds" for speculative profit-seeking. Due to the excessive interest requirements raised in the lawsuit, it was not until 2016 that the Argentine government paid off the principal and interest agreed with the "Vulture Fund" and regained the ability to borrow in the international market [7].

Although the 2001 external debt crisis is one of the worst debt crises in history, Argentina has recovered from this crisis at a faster rate than the long-term turmoil caused by previous external debt crises.

4.Strategies for Coping With Argentina's External Debt Crisis

For Argentina's external debt crisis, effective strategies can be developed from three aspects: debt restructuring and negotiation, optimizing debt structure, and economic structural adjustment and reform.

4.1.Debt Restructuring and Negotiation

The most direct way to deal with the debt crisis is to conduct debt negotiations with creditors and reach a new agreement. The Argentine government should consider the long-term and overall perspectives and avoid compromising with radical creditors such as "vulture funds" for short-term efficiency. Such compromises will not only increase future interest burdens but may also greatly increase the complexity of subsequent debt restructuring and negotiations. Therefore, the Argentine government should take the initiative to promote the improvement of relevant international laws and actively maintain the healthy development of the international debt negotiation system.

The significance of debt restructuring is to adjust debts so that the country's debt level matches its debt repayment capacity, while restoring international credibility to restore debt-raising capacity, providing operational space for subsequent solutions to the root causes of debt problems and enhancing the operability of economic reforms.

4.2.Optimizing Debt Structure

In terms of optimizing the debt structure, the primary task is to balance the currency structure of debt and reduce the excessive proportion of US dollar external debt. The Argentine government can develop a diversified settlement system by conducting currency swaps and settlement cooperation with major trading partners such as Brazil and China to reduce its dependence on the US dollar and alleviate the impact of US dollar exchange rate fluctuations on the Argentine financial system. Secondly, the proportion of short-term debt should be reduced. Although the borrowing difficulty and cost of short-term external debt are lower than those of long-term external debt, too much short-term external debt will lead to a concentrated repayment period and excessive repayment pressure. The Argentine government should rationally plan the structure of external debt maturity to reduce the risk of debt crisis.

4.3.Economic Structural Adjustment and Reform

The adjustment and reform of the economic structure should be regarded as the core means to deal with the external debt crisis. Argentina should adjust in both production and distribution. In terms of production, considering the large proportion of external debt, the government should change the single agricultural and animal husbandry export model [8]. On this basis, improve the domestic economic structure, optimize the resource allocation between the primary, secondary, and tertiary industries, promote the development of industrial production capacity and efficiency, reduce dependence on industrial imported products, enhance the endogenous driving force of economic development, reduce the balance of payments deficit, and increase foreign exchange reserves to improve debt repayment capacity and risk resistance. In terms of distribution, the government should adjust the structure of fiscal policy. Excessive welfare public expenditure has put too heavy a fiscal burden on the government. Therefore, welfare expenditure should be reduced while productive expenditure should be expanded. Improving financing support for domestic enterprises to stimulate economic development. All these contribute to fiscal self-sufficiency, thereby reducing fiscal deficits and dependence on external debt.

5.Conclusion

This paper analyzes the historical background and root causes of the 2001 external debt crisis and points out the relationship between debt and monetary system, fiscal structure, financial system, and development patterns. Although the imperfect financial system has contributed to the external debt crisis and expanded its negative impact to a certain extent, the root causes of Argentina's external debt problem are more likely to come from the unreasonable economic structure and the recurring fiscal problems. In the context of the lack of coherent economic policies due to political turmoil and frequent changes of government, the irrationality of production and distribution in the economic structure has aggravated the difficulty of managing the fiscal deficit, and the fiscal deficit problem has further caused inflation and debt problems, making Argentina's economic development problems spirally worse. Therefore, the key to solving Argentina's external debt crisis is to create space for the reform of the economic structure by restructuring debt and optimizing the debt structure. Then design a reasonable economic structure to improve the structural problems of production and distribution.

At present, Argentina's debt crisis still shows cyclical characteristics. This paper's discussion of Argentina's debt problem and the proposed solutions have positive practical significance and can provide useful reference and inspiration for the Argentine government to avoid potential debt crises. In the future, the Argentine government should continue to deepen economic reforms, strengthen cooperation with the international community, and jointly respond to global economic and financial challenges.